Speed Read:

- The FCA’s traffic light rating system changes the game for employer choice, but risks rewarding scale over quality. Standardised value for money (“VFM”) ratings give employers a meaningful basis for comparison for the first time, but the metric favours large, low-cost arrangements. Smaller, well-governed schemes with superior member support or sustainable investment options have limited means to demonstrate that value.

- The Mansion House Accord and the VFM Framework may pull in opposite directions. Schemes allocating to private markets may be penalised on both cost and performance metrics simultaneously, since private market returns lag and management fees are higher, even where the long-term risk-adjusted case is strong.

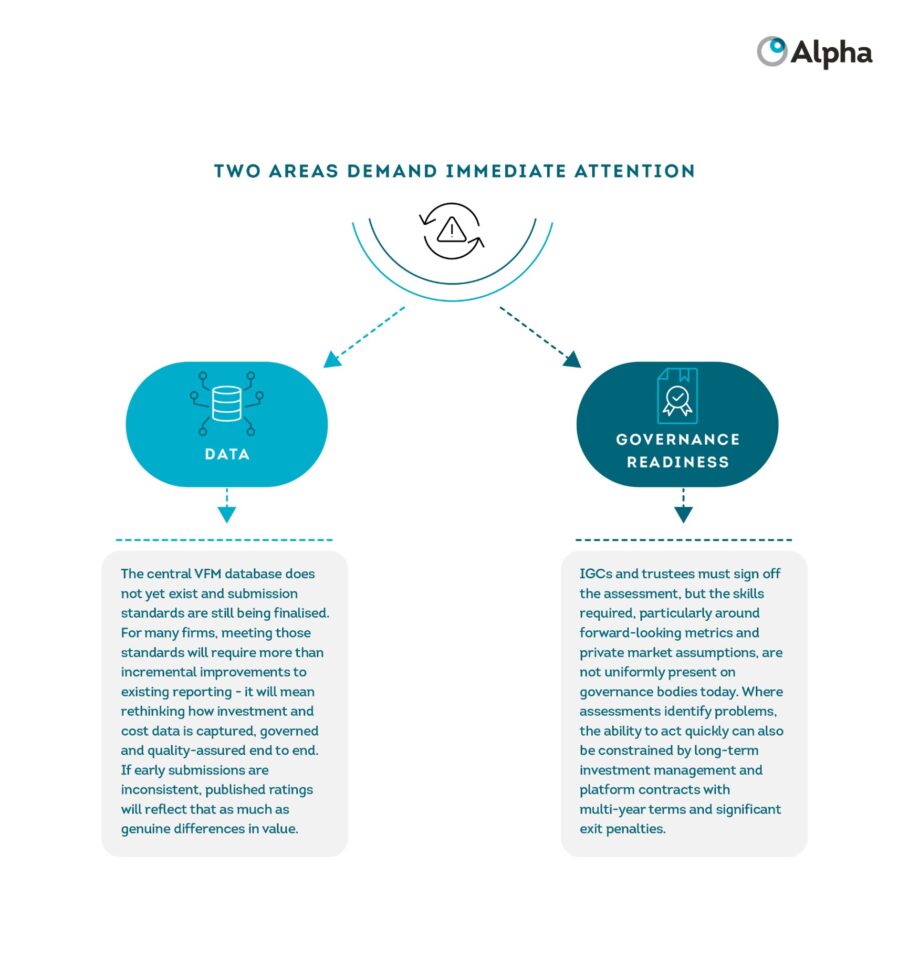

- 2028 is closer than most firms’ readiness suggests. Firms that underestimate the data infrastructure challenge will face boards signing off assessments built on foundations they cannot interrogate. Automated, auditable data pipelines need to be built now, not under deadline pressure.

- The framework has two structural blind spots: decumulation and member comprehension. Ratings stop at retirement, giving employers no signal on drawdown pathways or guided retirement journeys. Meanwhile, a simplified colour-coded label risks driving worse behaviour if members treat green as unambiguously good without understanding what the rating does not capture.

Introduction: The Value for Money Framework

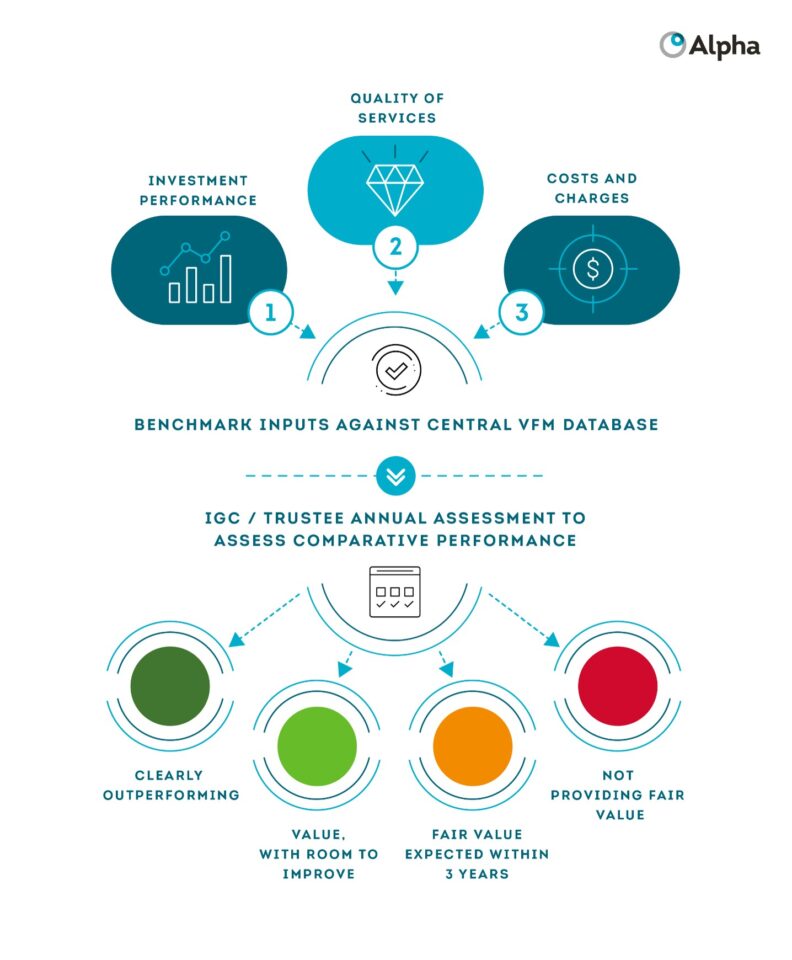

The FCA’s Value for Money Framework will require providers of workplace defined contributions (“DC”) default arrangements to measure and publicly disclose investment performance, costs and charges, and service quality against a standardised metric set, submitted to a central database for market-wide comparison.

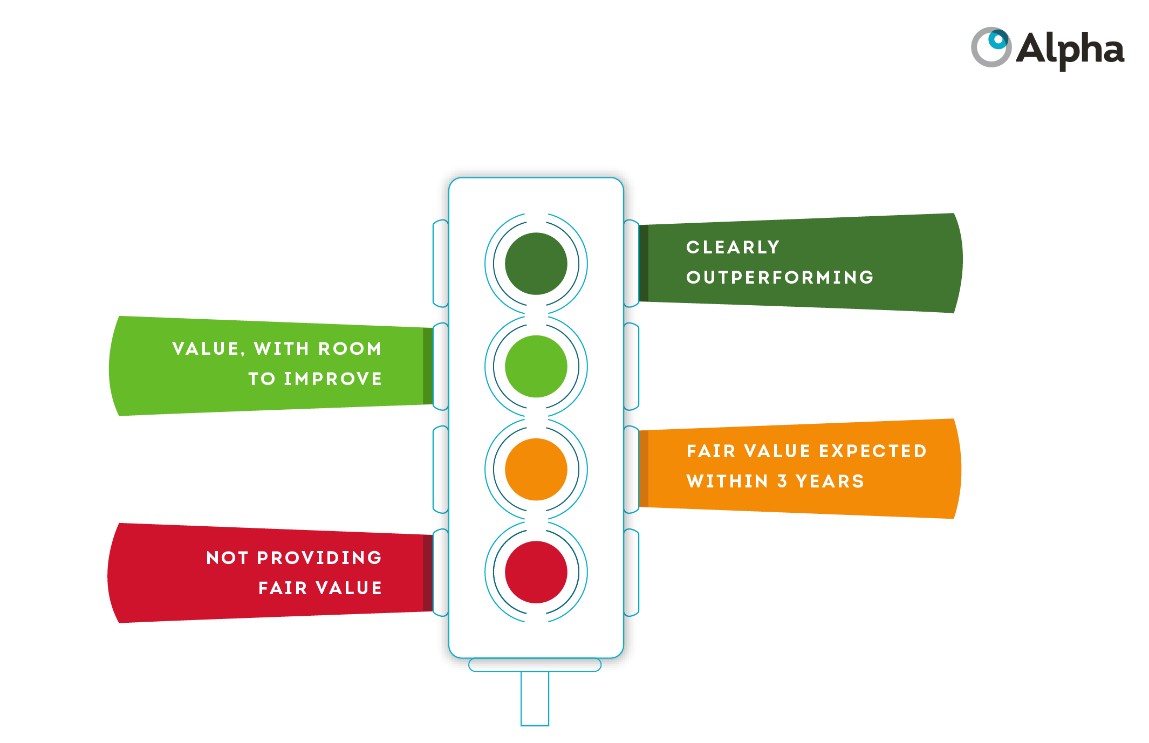

Independent Governance Committees (“IGCs”) and trustees must use that data to assign one of four public ratings.

Amber and red ratings may carry mandatory consequences – improvement plans, closure to new business, and ultimately member transfers using new contractual override powers proposed in the Pensions Schemes Bill. The first assessments are due in 2028.

Alpha is working with firms affected by the new rules. This note sets out our perspectives on the key consequences of the consulted rule changes.

The Traffic Light System

A publicly accessible, colour-coded rating is a genuinely useful addition to the market. Employers choosing pension providers have historically had little basis for comparison beyond cost; a standardised rating changes that dynamic in a meaningful way.

What does the rating actually capture?

In its current form, the metrics are heavily weighted toward cost and backward-looking investment returns. A scheme that is cheap and has performed well in the past will tend to rate well. A scheme offering sophisticated member support, sustainable investment options or high-quality digital servicing has limited ability to demonstrate that value through the current metric set.

The practical risk is that ratings accelerate flows toward the largest, lowest-cost arrangements – not because those arrangements are necessarily better for all members, but because the metric set favours them structurally. Smaller schemes, however well-governed, cannot replicate the cost economics of a master trust at scale. That is a question of size, not governance quality.

The framework explicitly contemplates that consolidation will follow, and firms of all sizes should be clear-eyed about what that means for them.

How VFM ratings are formed

Do the Framework and the Mansion House Accord Pull in Opposite Directions?

One of the sharper tensions sits at the intersection of investment strategy and ratings timing. The government’s Mansion House Accord asks schemes to allocate at least 10% to private markets by 2030. The VFM Framework assesses backward-looking performance over one-, three- and five-year periods. Unlike liquid assets, private markets are not continuously marked to market, which means reported performance lags and understates short-term volatility. A scheme making what it believes to be the right long-term allocation decision may, in the near term, look worse on published metrics than one that has not made that shift. Private market strategies also typically carry higher management costs, meaning a fund with private market exposure may be penalised on both the cost and the performance dimension of the rating simultaneously, even where the allocation offers superior long-term diversification and risk-adjusted returns.

The government's Mansion House Accord asks schemes to allocate at least 10% to private markets by 2030.

The introduction of forward-looking metrics in CP26/1 is a genuine improvement – the Association of British Insurers (“ABI”) has welcomed it specifically on these grounds, arguing it is vital to ensure schemes are not penalised for private market allocations where long-term value takes time to appear. But forward-looking metrics rely on market assumptions that are internally produced and inherently uncertain. For firms with meaningful private market allocations, building a credible and defensible methodology requires investment teams, governance bodies and external advisers to work together in ways that are not yet standard practice at most firms.

2028 is Closer than Most Firms’ Readiness Suggests

The firms that struggled most with Assessment of Value and Fair Value assessments under Consumer Duty made the same mistakes: they underestimated the data problem, built processes manually under time pressure, and ended up with boards reviewing assessments built on foundations they could not fully interrogate. VFM will repeat that pattern for firms that wait.

Government data suggests that around 77% of DC pension holders approaching retirement have no clear plan for how they will access their pension.

What the Framework Still Cannot Tell You

The framework has two structural blind spots that firms should factor into their planning.

How Alpha Can Help

Alpha is working with firms on VFM readiness across framework design and data infrastructure, including the governance and investment team collaboration that defensible forward-looking metrics will require.

If you would find it useful to discuss your situation and how others are approaching it, we would welcome a conversation so please get in touch.

About the Authors

Andrew Farrimond

Senior Manager

Andrew has more than seven years of financial services experience, including time at the Financial Conduct Authority. He has built expertise in operating model design across asset owners and asset managers, and has supported the design and implementation of a large UK manager's Value Assessment. Within Alpha, Andrew leads our Product and Conduct proposition, covering key regulatory change initiatives such as value assessments and Consumer Duty.

Amelia O’Hara

Consultant

Amelia is a Consultant within Alpha's Regulatory Compliance and Risk practice. She has developed experience supporting the delivery of a Global Compliance Framework Review and Enterprise TOM Implementation. Within Alpha, Amelia is actively involved in our Product and Conduct proposition, supporting firms to navigate regulatory change and embed best practice frameworks.

Chris Martin

Partner

Chris has more than 20 years of investment industry experience, including four years at the FCA across asset and fund management supervision. He has built a reputation for deep regulatory expertise, having also served as Head of Compliance and MLRO within industry. Within Alpha, Chris advises asset and wealth managers on compliance, risk and regulatory matters, drawing on nearly 10 years of consulting experience.

Nicholas Barbone

Senior Partner

Nick has over 15 years of advisory experience spanning Central Government and Financial Services. He has built a reputation for the definition and leadership of large-scale transformational change programmes globally across the asset and wealth management industry. Within Alpha, one of Nick's current responsibilities is leading our work with Asset Owners and Asset Servicers and further developing our market presence in these sectors.