Alpha FMC completed its third annual Global Operations Survey, drawing inputs from 75 Asset Managers and Asset Owners globally with a combined AUM of $28 trillion.

Speed Read

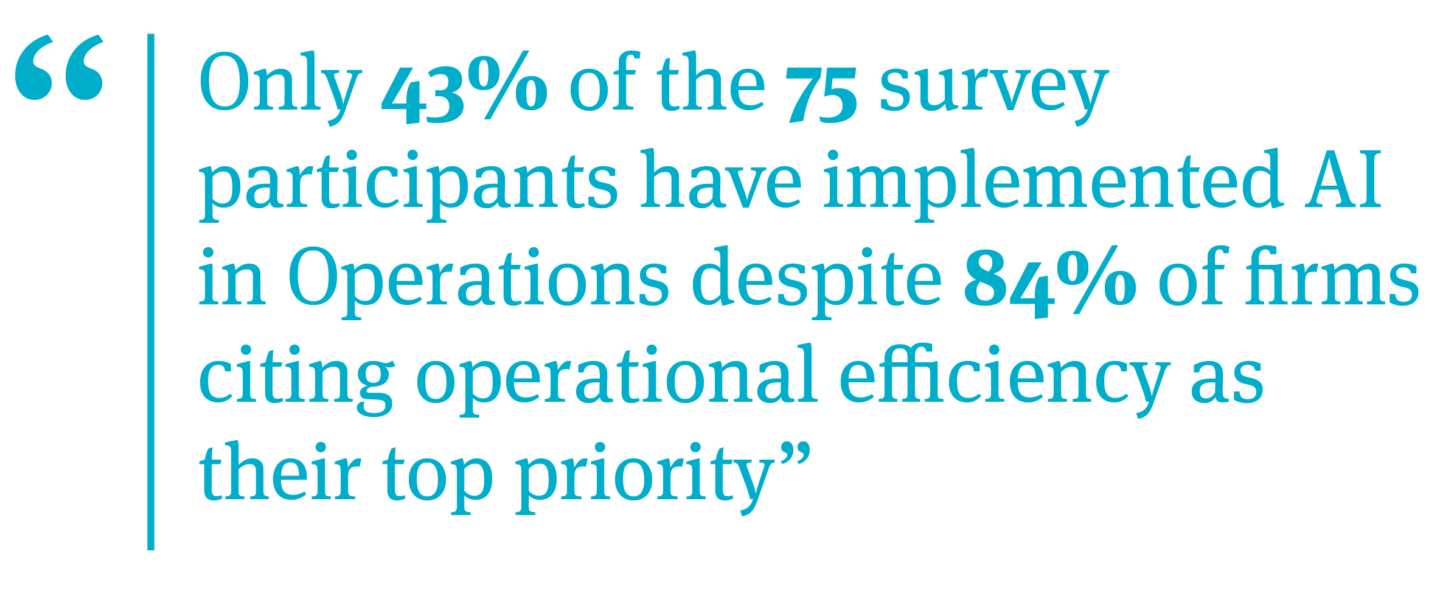

- AI is top of the agenda in Operations, but it’s still early. Only 43% of firms have implemented AI in Operations with limited transformational impact. 2026 is the year firms move from AI pilots into production use cases.

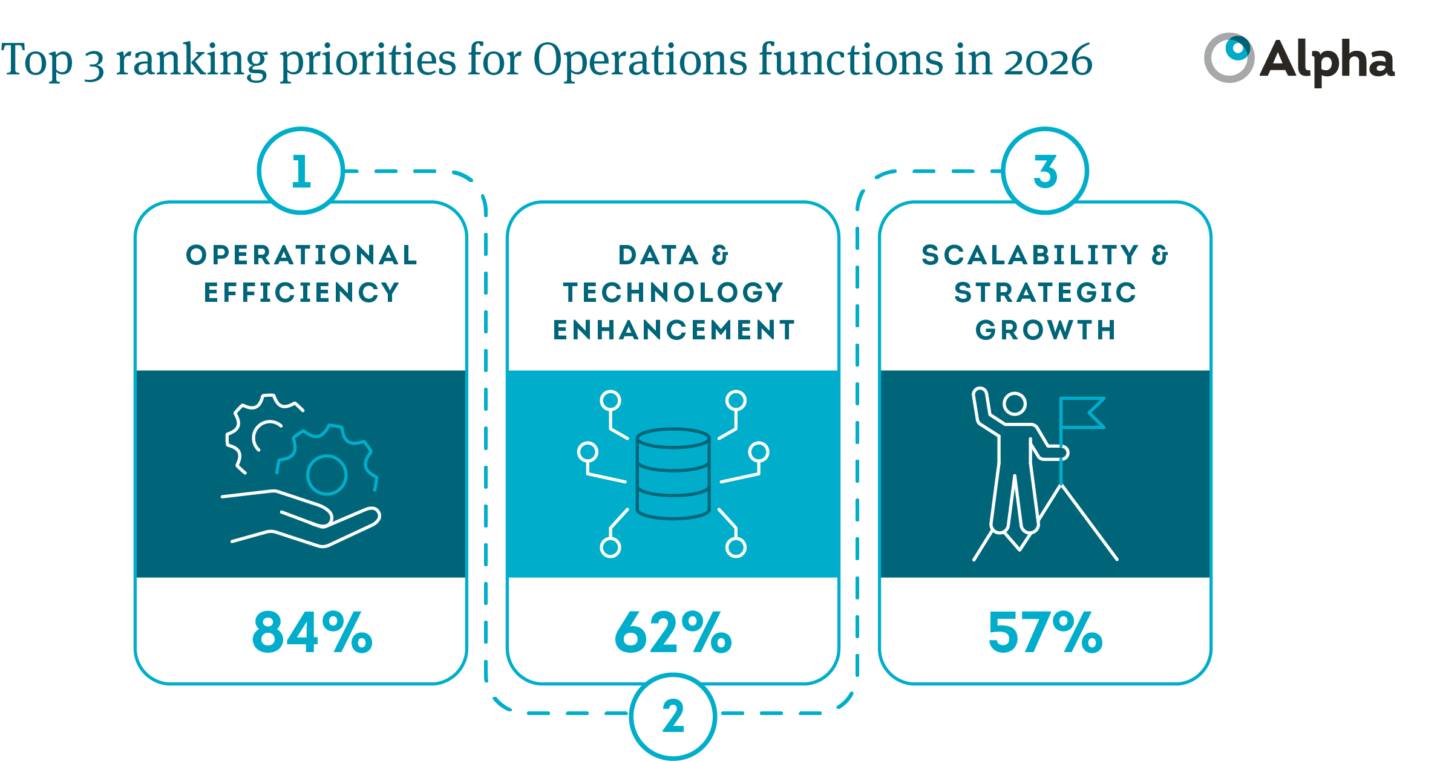

- Operational efficiency through AI and Automation is the number one priority for Operations functions, beating location strategy as a primary cost lever, with firms looking to automate before they relocate, targeting long-term scalability and management of cost alongside product expansion.

- Strategic initiatives replacing short-term cost optimization drives, firms undergoing cost optimization dropped from 61% (2024) to 51% (2025) as they shift from easy-access savings to structural efficiency gains.

- Outsourcing isn’t going anywhere Middle Office outsourcing continues to grow, 58% of firms partially or fully outsource Middle Office with Back Office consolidation continuing to accelerate. AI isn’t replacing outsourcing; they’re complementary initiatives.

Introduction: A shift from ‘cost out’ to driving operational efficiency through AI, automation and continued outsourcing

In an environment with continued margin pressure and evolving product complexity, Alpha’s current Global Operations Survey highlights how firms are sharpening their focus moving into 2026 to prioritize operational efficiency gains to support their growth trajectories whilst managing or maintaining their cost base. This is a notable shift from the 2024 survey findings whereby the focus remained on cost optimization initiatives, particularly through deliberate cost reduction.

In this article, we explore these three key themes that have emerged from the 2025 survey findings and how Asset Managers are shaping their 2026 priorities around these core areas including the use of AI in Operations, continued data & technology improvements and extending, or pursuing for the first time, outsourcing strategies to deliver scalability.

AI in Operations, shifting from ideation through to deployment into 2026

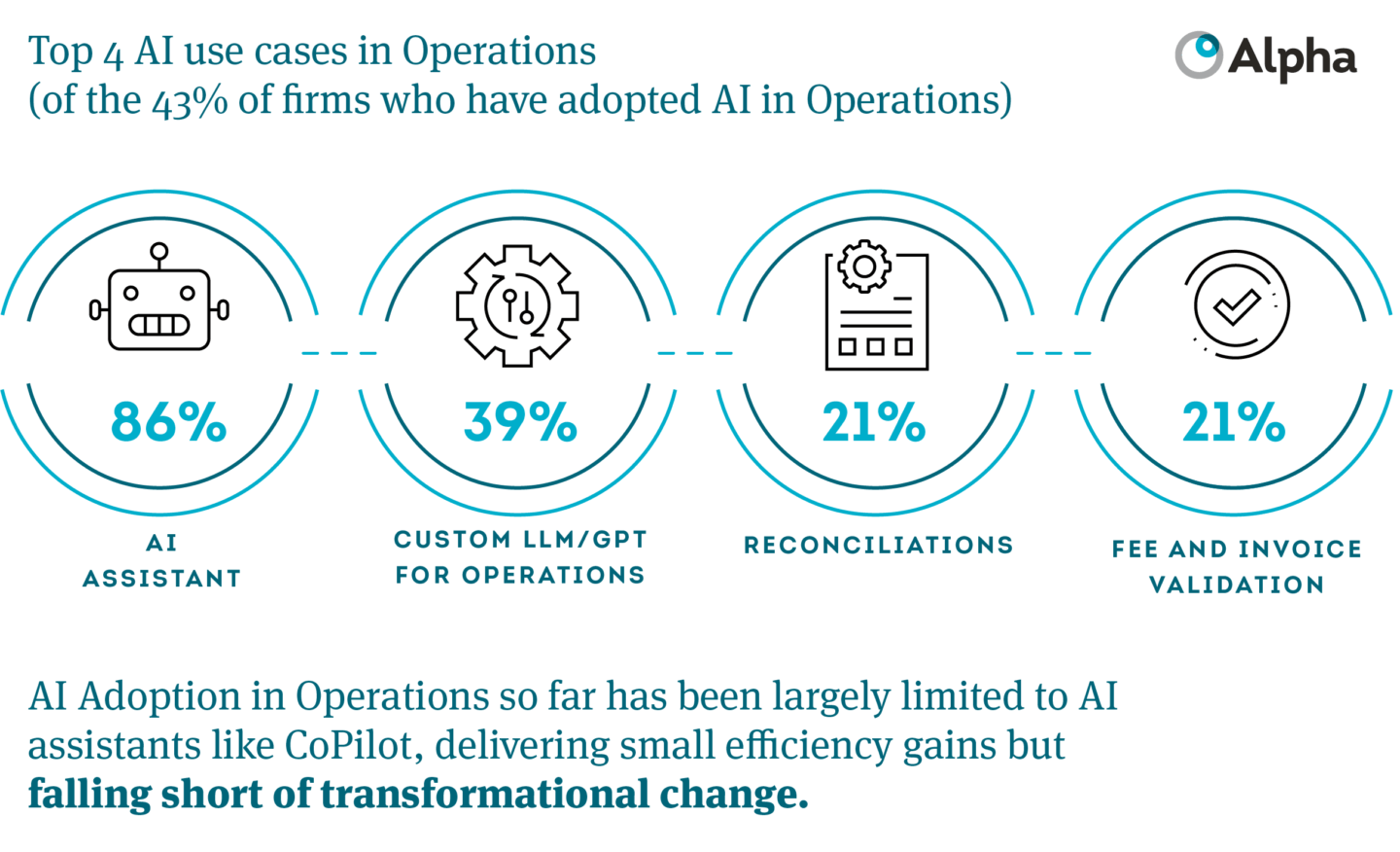

The Gap: Asset Managers continue to demonstrate meaningful AI success across Investment and Client functions, however Operations has lagged behind. Despite near‑unanimous agreement in survey responses on AI’s potential, the most common use case remains foundational AI assistance tools such as Copilot, used by 86% of firms that have adopted AI in Operations.

Why? Across firms of all sizes, participants cited data quality, shortages of AI-skilled talent, and integration challenges as the primary barriers to deeper adoption in 2025. Smaller firms remain more constrained, facing challenges around talent availability, cultural resistance, and split across buy, build, or hybrid approaches. Larger firms above $700bn AUM have moved early and decisively with 100% of firms having adopted AI in Operations.

What’s changing? However, moving into 2026, strategic partnerships between AI companies and Asset Managers have evolved, improving model capabilities, and alongside the emergence of Agentic AI, this points toward a material acceleration in adoption. From Alpha’s survey read-outs, firms are no longer just identifying use cases, firms are rapidly mobilizing pilots, proving value quickly and are actively driving AI adoption in BAU.

Data & Technology Enablement

In Alpha’s 2024 Global Operations Survey, we highlighted the continued rise in adoption of Cloud Data Platforms – a trend that has strengthened year on year. What began primarily within larger managers has now expanded meaningfully into the Asset Owner community and Asset Managers below $50bn AUM. These firms are accelerating the shift away from legacy and proprietary data environments toward cloud‑based platforms with dedicated operational data management capabilities. This year, we observed a 16% decline in the use of in-house or proprietary data platforms.

Adoption of data platforms remains closely intertwined with the use of Enterprise Platforms. While Enterprise Platform maturity has increased, now implemented by 55% of surveyed firms, technology selections are increasingly made in tandem with decisions around Middle & Back Office partners and data architecture. Notably, 18% of firms considering changes to their Middle Office outsourcing cited Enterprise Platform adoption as a primary driver.

Historically, technology, data, and outsourcing choices were made independently within functional silos. Alpha continues to observe a marked shift: these decisions are becoming more connected, more strategic, and more frequently elevated to the CEO and COO. Firms are increasingly recognizing that technology architecture, data strategy, and operational partnerships are no longer discrete decisions, but core components of an integrated operating model.

Despite continued Middle & Back Office outsourcing, service quality remains paramount

The levels of Middle and Back Office outsourcing have seen a year-on-year increase across the 2024 and 2025 Operations Surveys. Alpha has observed the size of firm, and propensity to outsource, with 69% of large firms and 48% of small firms fully or partially outsourcing their Middle Office.

This year-on-year trend to outsource does not seem to be slowing down; with 24% of firms seeking to increase the level of outsourcing across the Middle or Back Office, through two main areas:

- Continued increase in outsourcing of Middle Office functions

- Consolidation of Back Office providers

However, despite the focus on cost, operational efficiency and increased use of AI, the 2025 survey highlights that service quality always prevails in outsourcing decisions.

This highlights a more nuanced strategic approach to outsourcing. Firms are not focusing solely on cost but also service quality – consistency of service, responsiveness and alignment on key performance metrics highlighted as the key considerations.

Looking Ahead

As Asset Management firms continue to grow in both complexity and scale, Operations functions face mounting pressure to move beyond traditional cost‑reduction levers and embrace agentic AI and automation. The firms that differentiate and win through 2026 will be those that build operating models that are resilient, agile, data‑driven, agentic and automated, capable of supporting a broadening product mix while keeping Operations costs tightly controlled.

The Survey makes one point unmistakably clear: although AI adoption in Operations remains at an early stage, its transformative potential is no longer in question. Firms that successfully embed these technologies in 2026, supported by a modern data and technology stack and strategic outsourcing partnerships, will be best positioned to unlock meaningful efficiency gains, strengthen resilience, and manage their Operations cost base more effectively.

Alpha will launch its next Global Operations Survey this summer, with exclusive read‑outs provided to participating firms. If you would like to take part, please contact Alpha’s regional survey leads, who will begin engagement in June 2026.

About the Authors

Chyavan Rees

Partner

Chyavan is a Partner in Alpha's Operations practice who leads Alpha's Global Operations Survey. Chyavan specializes across Asset Management operations, including target operating model design, middle & back-office transitions, enterprise transformations and client reporting. As part of the Global Operations Survey Chyavan leads engagement with Alpha's UK participants, discussing survey findings, industry trends and the future of Operations with a range of Asset Managers.

Bastiaan Aalders

Senior Partner

Bastiaan is a Senior Partner with over 25 years of experience in the Financial Services sector. He leads Alpha’s European Operations practice and oversees Alpha AWM in the Netherlands, Belgium, and the Nordics. With a deep understanding of the Asset Management industry, Bastiaan is well-versed in intricate front-to-back operating models. He recognizes the evolving landscape, both functionally and technically, and is adept at navigating these changes.

Suzanne Meador

Director

Suzanne is Director and leads our North American benchmarking practice. Suzanne has over 25 years of financial services experience predominantly working for TPA’s in leadership roles with a focus on pricing, profitability and strategy; most recently at BNY as the Global Head of Asset Servicing Pricing and Profitability. She has significant experience and knowledge of market pricing practices, operating models and service provider offerings. Suzanne has led a variety of tariff, service, vendor oversight and insourced cost benchmarking engagements since joining Alpha last year.