Context

Client attrition is a normal phenomenon in any business and Wealth Management is no exception. However, Wealth Managers have somewhat overlooked attrition, often treating it as an acceptable ‘cost of doing business’.

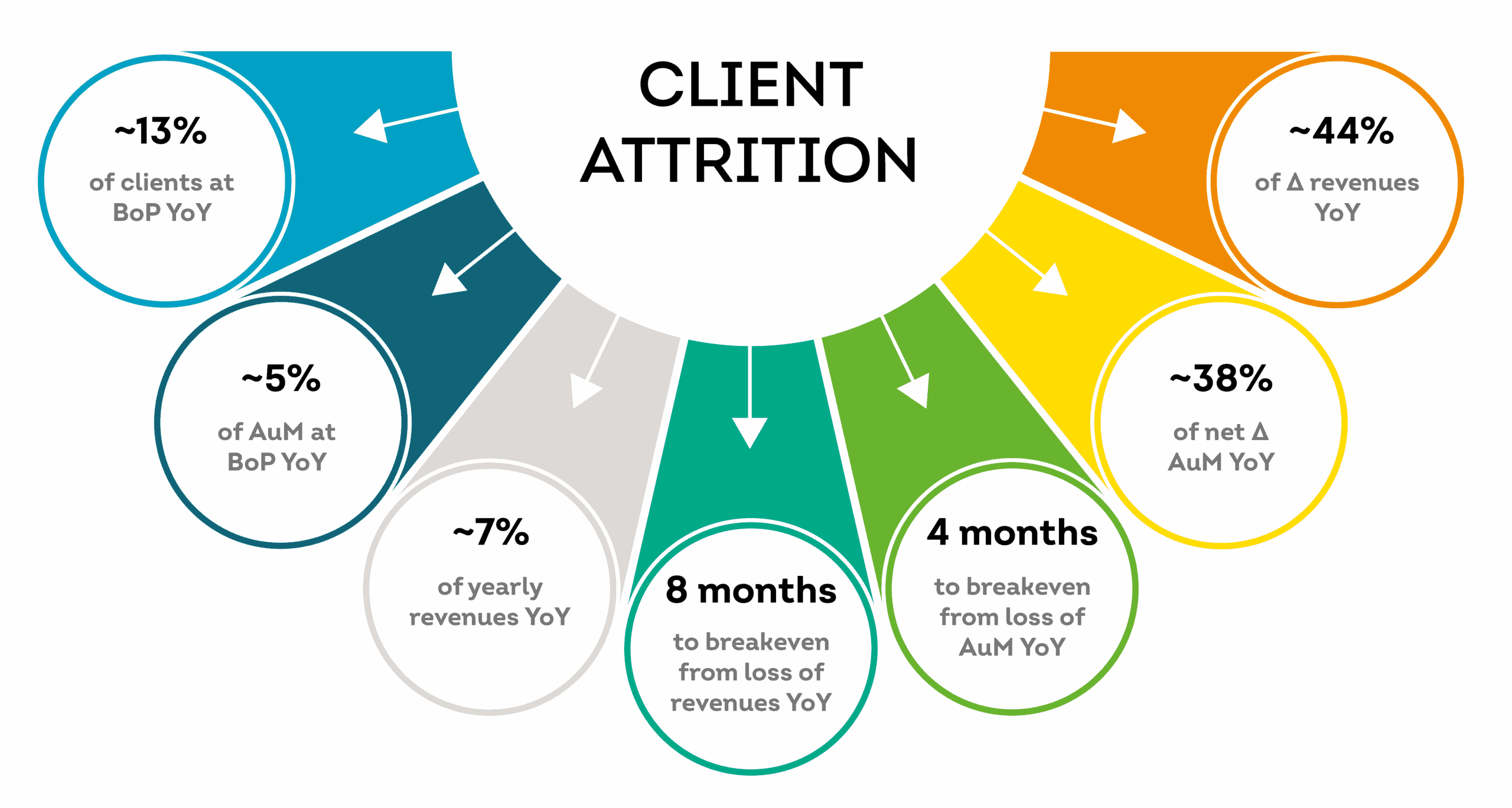

For context, attrition is typically material – at any time 10-15% clients and 5-10% of revenues may be at a relatively high risk of attrition and 4 to 8 months[1] of growth are ‘used’ just to break-even[2] from undesired client churn in any given year (see Figure 1).

Note: BoP stands for Beginning of Period

Source: Case studies based on previous project experience

Attrition is also preventable, over 50% of its common causes can be addressed by Wealth Managers if Relationship Managers (RMs) are better informed of the individual attrition risk associated with each of their clients.

Finally, attrition is relatively prevalent among the RM population, it is not uncommon to find that ~50% of RMs account for ~80% of lost clients.

Key in explaining attrition is the limited awareness RMs possess concerning clients at risk. While some of this limited awareness results from the relatively limited emphasis placed by senior management (consequently RMs) on the topic, a significant portion is due to clients not ‘speaking out’ until it is too late.

Despite the lack of explicit communication, clients’ reduced satisfaction becomes evident through their behavior during a phase of ‘neglect’ (prior to an ‘active exit’ phase) in which clients seek a resolution and assess their options.

Approach

We consider client attrition as a topic where Artificial Intelligence (AI) can be used to develop predictive models, designed to identify clients at risk and to provide that information to RMs, who can then take appropriate retention measures where merited.

AI algorithms are particularly well-suited to identify the behavioral changes of clients at risk that normally occur during the ‘neglect phase’ of attrition.

Since clients are heterogeneous, there is no ‘silver bullet’ to accurately predict attrition. Instead, it is the cumulative weight of various behavioral indicators, ranging from relationship dynamics and communication patterns to trading activities, that creates the foundation of evidence for risk levels.

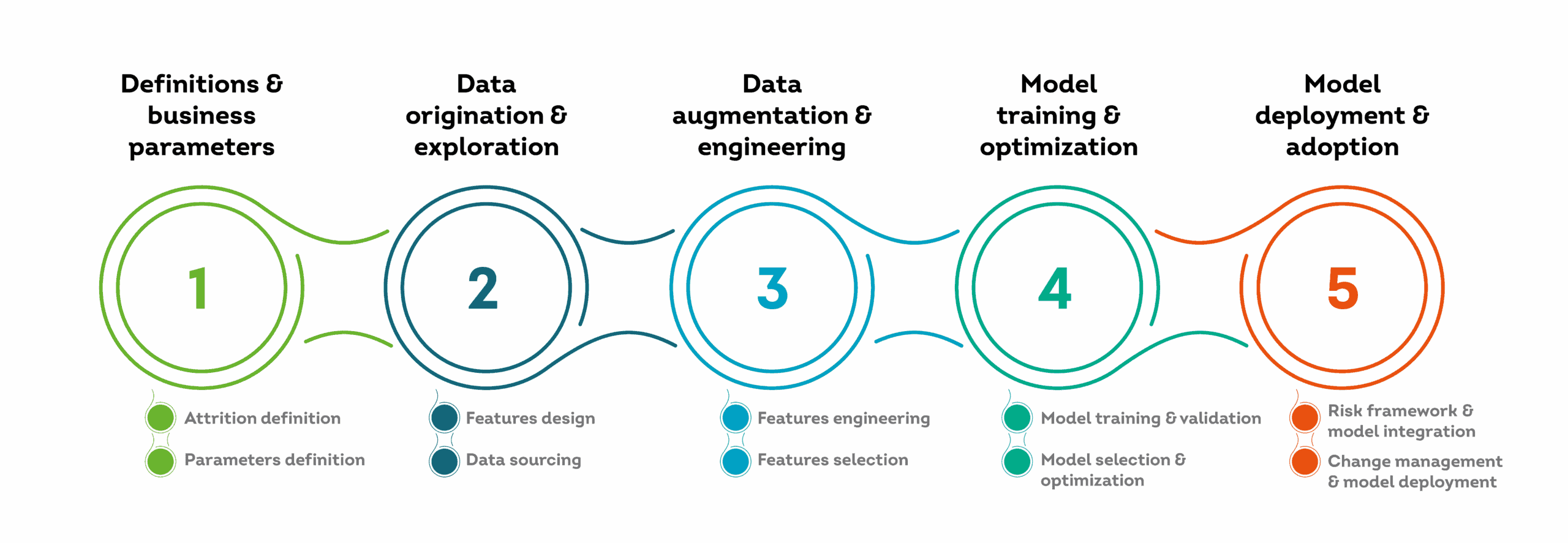

While the steps involved in developing AI-enabled attrition models are similar to those of most other AI use cases (see Figure 2), in our experience, three aspects are key in terms of creating usable models:

- Definition of key business parameters, comprising a clear definition of what a client is, what attrition is, the ‘observation’ period (in which client behaviors are observed) and the ‘outcome’ period (where we look to predict client churn).

- Engineering of descriptive features, comprising the creation of ‘longitudinal’ features that accurately describe temporal shifts in behavior – typically, these features account for 40% to 50% of the algorithms’ predictive capability.

- Optimization of the predictive model, comprising the calibration of the predictive model to business rather than merely technical criteria. This is relevant since different types of errors carry different business impacts (false negatives may represent a total revenue loss).

Upside

While, attrition algorithms require a significant amount of data, especially historic data, the type of data used is mostly plain vanilla, internal structured data. Additionally, structured market data is commonly integrated for context.

The primary data-related challenge, typically comes from the relatively limited number of departing clients compared to the materially larger population of retained clients year-on-year. This can severely unbalance datasets and requires specific mitagation actions.

To counteract this, our approach looks to identify clients that left in previous years and then gather the relevant data for those. This could entail gathering 15 months’ worth of historical data from the point of client churn.

Ultimately, addressing client attrition yields both ‘defensive’ and ‘offensive’ benefits in that it can:

- Prevent the loss of clients, assets and revenues worth 2 to 5% in ‘retained revenues’;

- Offset the opportunity costs of less satisfied clients worth 3 to 7% in ‘incremental revenues’.

Collectively, these impacts represent approximately 9% of revenue potential that could be realized if Wealth Managers proactievly tackle client attrition.

Considering the potential investment needed to address attrition, this type of initiative is likely to carry an ROI of 15 to 25%, although this is contingent on the individual Wealth Manager’s starting point.

How can Alpha help?

We have extensive experience in successfully developing and deploying AI-enabled attrition models. We would welcome the opportunity to discuss the importance of this subject, its underlying causes in your specific context, and share out experience on effective strategies for addressing it.

Please do get in touch to find out more about how Alpha can help.

Footnotes:

[1] Of asset and revenue growth respectively

[2] From previous year’s unwanted attrition